Firstly, let me be clear…this is not a payments story. It is very interesting though!

Apple just reported the biggest quarter of net income earned by any public company ever, at least in nominal terms. It remains the world’s most valuable publicly traded company by a large margin. So naturally there are people who want to put these statistics into perspective by comparing a corporation to a country. Unfortunately, most of those efforts miss the mark because they generally don’t compare apples to apples – reports Matthew Klein in the FT.

The most common way to measure the size of an economy is to look at how much stuff is produced in it each year. (This is GDP.) You might think that is equivalent to corporate revenues, except that a lot of those inflows are offset by outflows to suppliers. In other words, you’d be looking at a company’s GDP without subtracting the imports that represent foreign production. That’s double counting.

To get around this problem, remember that the value of all the stuff a country produces ought to equal the amount of money everyone in that country gets paid (before taxes, and including net interest) over that same period. At the country level, you can think of this as basically equivalent to gross salaries and benefits plus profits. At the company level, it is the sum of employee compensation and EBITDA. (That sum represents the gross value added by Apple, which is the best analog to GDP you can get.)

We ran the numbers with Apple, although we had to do some guesswork to calculate employee compensation. The company doesn’t break out the numbers, except for share-based schemes, so we added “sales and general administrative expenses” to research and development spending to use as a rough proxy. We left out the “cost of goods sold” even though it may include some employee pay because all the components and manufacturing of Apple’s products are done by suppliers. As it happens, our methodology produces results similar to this estimate of Apple employee compensation that the company sponsored a few years ago.

First, let’s look at how much economic value Apple has been creating:

The chart shows the estimated, rolling four-quarter sum of Apple’s gross value added.

Apple enjoyed rapid and accelerating growth in its economic output until sometime in the second half of 2012. Then growth abruptly stopped and Apple entered a mild recession that lasted until 2014. It returned to growth sometime last year, albeit at a slower pace than before.

Fittingly, Apple’s share price seems to have broadly mirrored this action. The stock peaked in early September, 2012, sank by almost half by the middle of 2013, gradually rose, and then went off on a tear starting in the spring of 2014.

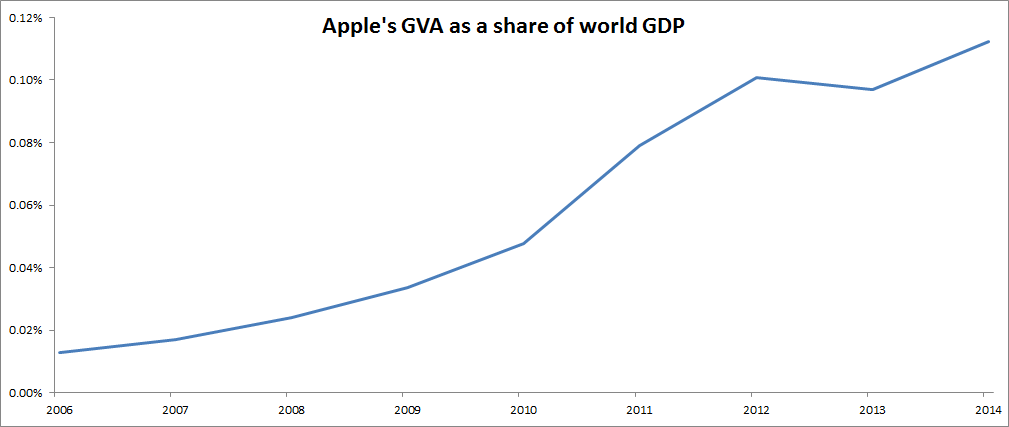

How does this compare to other countries? The next chart combines our numbers with the International Monetary Fund’s estimates of global economic output to put Apple into perspective:

To be precise, we estimate that Apple’s economic output in 2014 was worth about $87 billion. According to the IMF, the next biggest economies were Ecuador and Slovakia, which each produced about $100 billion. Just below Apple were Oman at $81 billion, Azerbaijan at $78 billion, and Belarus at $77 billion.

The Apple economy grew much more rapidly than the world economy over the past few years, as you can see in the next chart, which compares Apple’s output to global output:

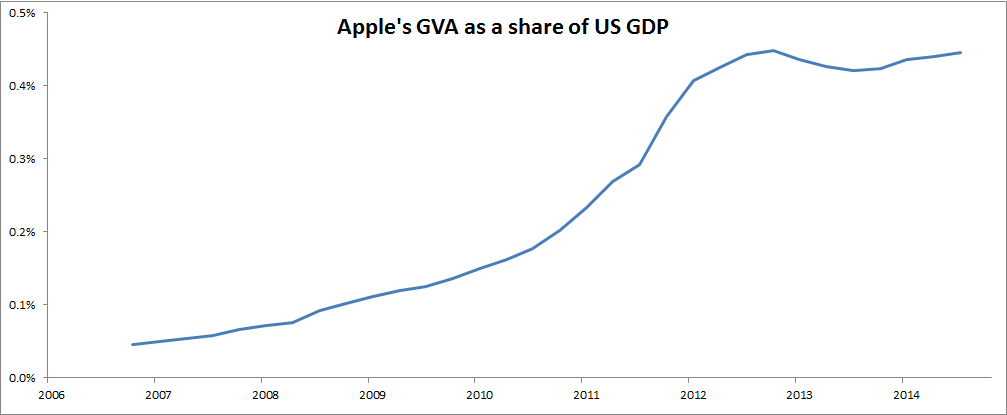

A little more than one one-thousandth of the world economy is Apple. As a share ofUS GDP, Apple is a bit bigger but seems to have stagnated since peaking at the end of 2012:

Another topic that gets a lot of attention is Apple’s sizable holdings of liquid assets. These aren’t remotely comparable to a country’s GDP, but they could be usefully compared to a foreign exchange reserve or sovereign wealth fund.

After all, every company, including Apple, has its own unique currency it can use to make acquisitions and pay employees — its shares. Companies can manage the supply of their currency by issuing and buying back stock, which is basically the same thing as printing or destroying money. That in turn affects the exchange rate (earnings multiple) of its currency against both hard currencies and other corporate equities.

Like emerging market countries, Apple has hard currency liabilities that it can’t print its way out of. (Not just debt but also supplier contracts, employee salaries, etc…) Apple gets paid in hard currency, which helps, but compared to most countries, its economy is extremely concentrated on a few products. That makes it more analogous to, say, a small petrol state than a diversified economy like Slovakia.

When well-run countries find themselves in this situation, they generally consider a portion of their commodity earnings as windfall profits that get invested in foreign reserves and the sovereign wealth fund. These reserves can be drawn upon to defend their currency and maintain purchasing power if their terms of trade deteriorate.

Apple and other big tech companies behave similarly, retaining some of their hard currency earnings in liquid assets. When Apple’s exchange rate share price collapsed in 2012, activist investors pushed the company to draw upon these reserves to defend the currency use the cash for buybacks.

Apple presumably learned from that experience, which is why it currently has about $178 billion of liquid assets on its balance sheet. While these assets have grown rapidly in size, they have been pretty stable relative to Apple’s annual economic output — about two years of Apple’s GVA.

Taking the the Sovereign Wealth Fund Institute’s list of big funds and compared it to the IMF’s GDP estimates, we find that Apple’s reserves are about the same relative size as Norway’s. For comparison, Kuwait’s sovereign fund is worth about three years of economic output, UAE’s funds are worth about two-and-a-half years, while Saudi Arabia’s sovereign savings fund is worth about one year.

Hopefully this exercise helps put the size of the world’s most profitable and valuable company in the proper perspective.

The post If Apple were a country… appeared first on Payments Cards & Mobile.