The strong performance was driven by the lowest level of risk costs on record, according to the Kearney 2022 Retail Banking Radar, with the predicted wave of COVID-related loan defaults being mitigated by proactive policies from governments and banks.

However, not a lot changed in bank performance and business fundamentals. While retail banks averted the severe consequences of the pandemic, underlying business indicators—such as revenue per client and cost-to-income ratio (CIR)—did not change significantly.

Retail banks have benefited over the past decade from changing customer behaviours and took the opportunity to decrease the number of both branches and employees. Yet, finding ways to decrease costs even by 1 to 2 percent a year from now on—after a reduction of 25 percent of branches and 12 percent of employees in the past five years alone—will be increasingly difficult.

While 2021 surprised on the upside, the outlook is uncertain. On the one hand, rate increases from the European Central Bank (and other central banks) and the end of the more than decade-long zero-interest-rate policy could provide a boost to bank revenue through an improvement in net interest margins.

On the other hand, with inflation hitting multi-decade highs in most of the EU and the UK and with household incomes being squeezed, closely managing costs will remain a key topic for banks. Yet, another windfall—akin to the 2021 provision release— is unlikely.

A structured and disciplined transformation of operating models is the main lever retail banks have in their hands to manage through upcoming times of economic difficulty and turmoil.

European banks – Spectacular recovery

Pent-up demand and a reversal of risk costs helped European banks perform more robustly than it looked like at the beginning of 2021.

Our 2022 Retail Banking Radar shows that profit per customer across Europe as a whole leaped 43 percent to €214 in 2021 compared with €150 the prior year—the highest figure since 2016. Out of the 21 countries analyzed, Italy and the UK led the way, while only banks in Poland saw their profit per customer drop.

This substantial profit rebound was heavily linked to noteworthy drops in provisions and, to some extent, revenues recovering from the 2020 trough.

Our analysis shows that banks in every one of the 21 countries witnessed falls in risk provisions as a percentage of income, with Italy’s 19.5 percentage point drop being the second highest out of all countries studied and the UK at third with 21.1 percentage points (see figure 1).

Both were behind Poland’s outsized 29.6 percentage point fall, which helped the Eastern Europe region outperform its peers with a 17.0 percentage point fall, narrowly above Southern Europe’s 15.5 percentage point drop but well ahead of Western Europe’s 9.0 percent reduction.

Twelve out of the 21 countries registered a rise in income per customer, with the UK notching up the second-highest increase at 5.1 percent. The Nordics and Switzerland region produced the biggest rise out of the regions covered (4.1 percent) while Eastern Europe eked out growth of 1.1 percent.

This income growth largely made up for lost revenues in the first year of the pandemic. It also meant that the CIR fell slightly in 14 out of the 21 countries in 2021 (see figure 2).

Assessing the picture by region, Western Europe produced the biggest drop (-1.9 percentage points) thanks to robust performances from the UK and Austria (-5.4 and -2.7 percentage point falls respectively), while Portugal’s -3.1 percentage point drop led the way in Southern Europe, which nevertheless posted a 0.5 percentage point increase.

Running to stand still

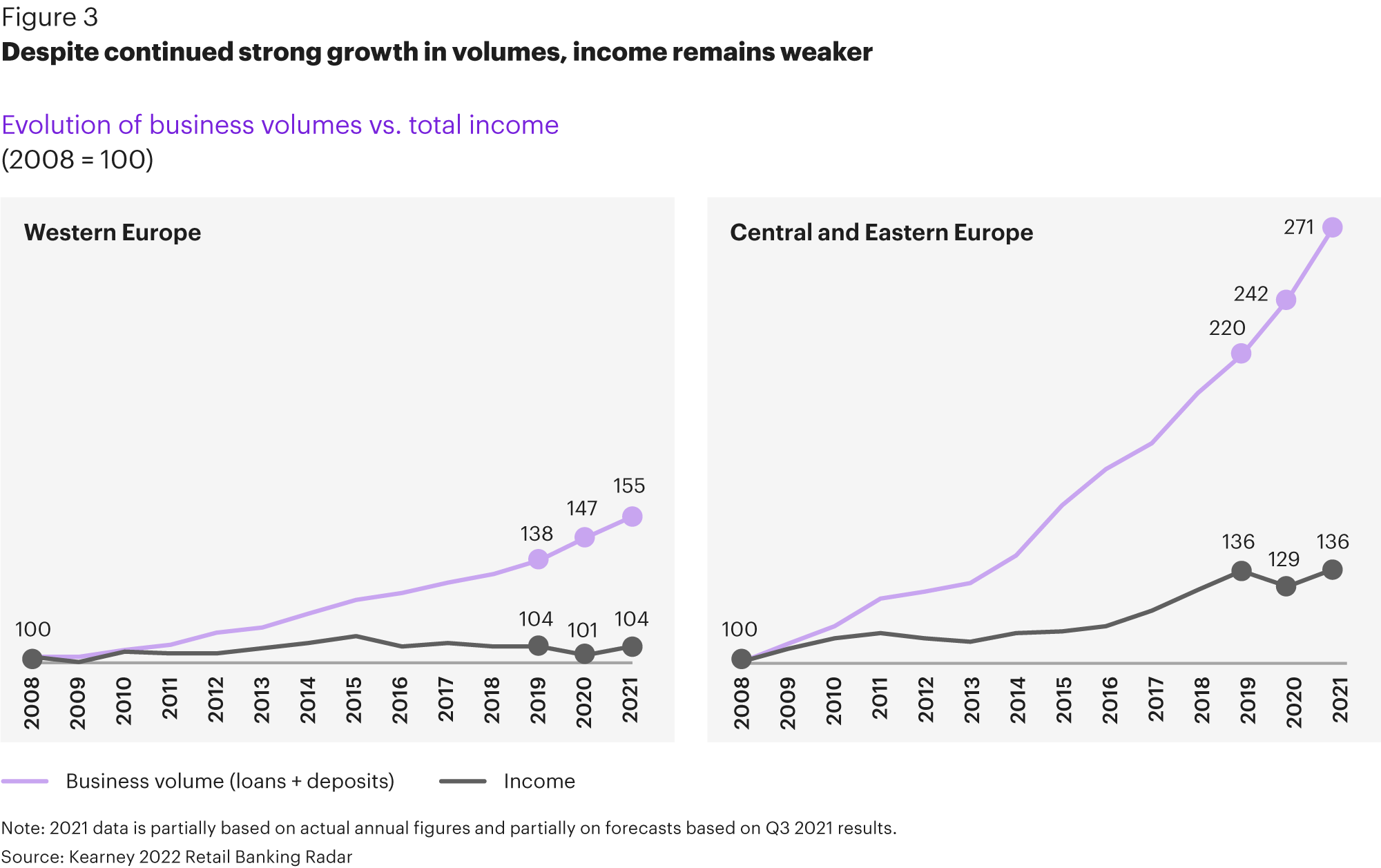

Despite several crises during the past 15 years—the 2008–2009 global financial crisis, the European sovereign debt crisis in 2011–2012, and not to forget the COVID-19 pandemic, the retail banking sector remained resilient (see figure 3).

The growth in loan and deposit volumes was uninterrupted in the past 15 years and peaked in the past two years, up 6.8 percent in 2020 and 5.5 percent in 2021 compared with a 3.1 percent average.

For the banks covered by the Retail Banking Radar, loan volumes were up 4.3 percent, with Eastern Europe leading the way with a 9.6 percent rise, followed by Western Europe’s 4.1 percent.

Deposits leaped 6.6 percent as households and small businesses saved more as a result of the economic uncertainty created by the pandemic. Eastern Europe again outpaced the other regions with 13.3 percent growth in savings, and Southern Europe was next with 10.9 percent growth.

Despite the strong rise in business activity, retail banking revenues for Europe as a whole were broadly flat compared with 2019, suggesting that banks have had to run at pace just to stand still.

Over the same period, banks have become more productive. These higher business volumes are being supported by fewer employees and a smaller branch footprint.

The branch network in Europe has declined by 25 percent since 2016, particularly in Eastern Europe and Southern Europe with reductions of 27 percent and 26 percent respectively. Banks have also trimmed their headcount by 12 percent in the past five years while supporting a 25 percent increase in business volumes (see figure 4).

Every region analysed in the Radar has improved its productivity thanks to these factors, with the Nordics and Switzerland region witnessing business volumes grow by more than half (54 percent), followed by Eastern Europe’s 28 percent. Even though Southern Europe reduced its employee count by the most out of any region studied (20 percent), its business volumes have only grown by 11 percent since 2016.

The UK led the way with a 16.6 percent rise in income per employee—the highest of any country surveyed—while Spain led Southern Europe with a 10.3 percent rise.

European banks – Battling costs

Retail banks have closed branches and proactively reduced their headcounts in a bid to streamline their operations and respond to the increasing digitalization of the sector—moves that have created financial challenges as well as opportunities.

However, our research shows that only Southern Europe cut costs in 2021, while they rose in Western Europe, the Nordics and Switzerland, and Eastern Europe by 1.1 percent, 2.1 percent, and 5.5 percent respectively (see figure 5).

Although banks significantly reduced their headcount and branch network, savings from those initiatives haven’t flowed through to the bottom line, primarily because of three factors: wage inflation, technology spend on digitalization, and higher compliance spend.

Two years ago, we said European retail banks would need to reduce costs by €35 billion to €45 billion over the next three to five years to meet their profitability targets. Our research shows that retail banks collectively have realized no net cost savings. In fact, 45 out of the 89 banks in our database have seen costs go up since 2019.

In our opinion, most of the easy cost savings have been delivered through the branch and headcount reductions. While some banks or regions might still have potential to do more in these two areas, delivering sizable cost savings is becoming a lot more difficult.

To create more efficiency gains, banks need to revamp their operating models to become digital first—not only in their customer-facing activities but also in how they run their day-to-day operations.

Taking control, not only surviving

While these figures demonstrate the sector’s resilience and its ability to navigate challenging environments, there are dark clouds on the horizon. A looming recession across most of Europe flags caution for 2022.

Inflation in Germany recently hit a four-decade high for a single month, while prices rose in February at their fastest rate in a 12-month period since records began in 1997. The Bank of England is predicting that inflation will exceed 10 percent by the end of this year.

With consumer confidence and retail spending beginning to decline, the demand for banking products could also soften, and it will be imperative for the sector to monitor how the rising cost of living might impact prospects for rising loan defaults and an increase in risk costs.

There might be a silver lining: interest rate rises in Europe and the UK could lead to an increase in net interest margins for the industry. However, given the uncertain outlook, retail banks will have to make tough choices in 2022 (and potentially beyond).

Additional investments will require some level of cost reduction, which is no longer possible to fund without a structural change of operating models. Now is the time for retail banks to take control of their destiny and act.

The post European banks show excellent COVID recovery and record profits appeared first on Payments Cards & Mobile.